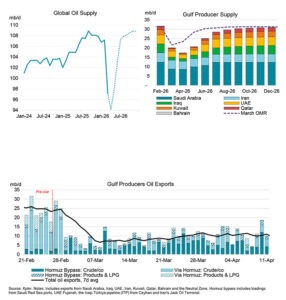

The global energy landscape faces an unprecedented crisis as the ongoing conflict involving Iran sends shockwaves through international markets. The International Energy Agency released its latest Oil Market Report on April 14, 2026, revealing the most severe supply disruption in history. Relentless attacks on critical energy infrastructure across the Middle East and severe restrictions on tanker movements through the Strait of Hormuz caused global oil supply to plummet by 10.1 mb/d, landing at 97 mb/d in March.

Global Oil Supply Plummets as Middle East Conflict Triggers Historic Market Shock

This monumental drop in production completely alters the economic outlook. Analysts now project that global oil demand will contract by 80 kb/d this year. This figure represents a staggering 730 kb/d downward revision from the forecast published just one month prior. Experts anticipate a massive 1.5 mb/d decline in the second quarter of 2026 alone. The report notes this plunge marks the sharpest drop since the global pandemic slashed fuel consumption worldwide.

The crisis immediately triggered panic across trading floors and drove prices to record heights. North Sea Dated crude recently traded near $130 per barrel, representing a massive $60 per barrel premium over pre-conflict levels. The International Energy Agency stated, “The Iran war upends our global outlook.” The agency further warned that this severe supply shock forces major economic realignments as nations scramble to secure increasingly scarce energy resources.

Unprecedented Production Losses

The Organization of the Petroleum Exporting Countries and its allies suffered massive production losses. OPEC+ production fell 9.4 mb/d month-over-month to 42.4 mb/d. The conflict paralyzed major extraction facilities across the region. Non-OPEC+ supply also declined by 770 kb/d to 54.7 mb/d. Lower Qatari output drove this specific drop. Production gains in Brazil and the United States partially offset the Qatari decline.

However, these American and South American increases cannot cover the massive Middle Eastern shortfall. Global crude throughputs continue to struggle heavily. Disruptions to feedstock supplies and severe infrastructure damage cause these struggles. These factors tightly squeeze global product markets. Refineries currently operate at only 65% of their total capacity. The market effectively lost nearly 10% of its total daily supply.

Regional Demand Destruction

The deepest cuts in oil use initially hit the Middle East and the Asia Pacific. Regional consumers drastically reduced their consumption of naphtha, LPG, and jet fuel. The International Energy Agency offered a grim warning about the future. The report stated, “However, demand destruction will spread as scarcity and higher prices persist.” Skyrocketing prices force ordinary citizens and major corporations to slash their energy use. Refineries in the Middle East and Asia face severe feedstock constraints.

In April, these constrained refineries cut runs by around 6 mb/d to 77.2 mb/d. Analysts expect global crude runs to decline by 1 mb/d on average in 2026. The industry projects a total average run of 82.9 mb/d for the year. Refining margins temporarily surged amid the chaos. Middle distillate cracks reached all-time highs as the crisis deepened. Middle distillate prices in Singapore surpassed $290 per barrel. This represents a catastrophic cost increase for commercial transportation and aviation sectors.

The Strait of Hormuz Bottleneck

The Strait of Hormuz acts as the primary chokepoint for global oil logistics. Ongoing restrictions choke off essential vessel movements. The report confirms that these restrictions created the largest disruption in history. A recently announced United States blockade targets vessels entering or departing Iranian ports. This blockade further complicates an already volatile maritime shipping environment. Shippers cannot move products through traditional channels.

Global observed oil inventories fell by 85 mb in March. Stocks outside the Middle East Gulf saw a significant drawdown. Refineries depleted these external stocks by 205 mb. This drop equals roughly 6.6 mb/d. Nations draw heavily from their strategic reserves to maintain basic operations. Market analysts watch these declining stockpiles with intense concern.

Surging Floating Storage

Producers inside the Middle East face a completely different inventory problem. They have extremely limited outlets after the effective closure of the Strait. Floating storage of crude and oil products in the Middle East rose rapidly. Companies added 100 mb to floating storage vessels. Onshore crude stocks in the region also increased by 20 mb. The oil simply has nowhere to go. Tankers sit idle in the Persian Gulf. Meanwhile, other nations desperately hoard whatever resources they can secure. China aggressively purchased available supplies to bolster its national reserves. The Asian economic powerhouse added 40 mb of crude to its tanks. They utilized the chaos to secure long-term strategic supplies.

Historic Price Shocks

March 2026 witnessed unprecedented financial volatility in energy markets. Oil prices posted their largest-ever monthly gain. Spot crude benchmarks and differentials soared to staggering new heights. These spot prices quickly outpaced futures markets. Refiners anxiously scrambled to replace locked-in Middle Eastern cargoes. Desperation drove buyers to pay massive premiums for immediate delivery.

The market dynamics shift hourly as new intelligence emerges from the conflict zone. A brief two-week ceasefire between belligerents provided some temporary market relief. However, analysts doubt the viability of a lasting negotiated settlement. The International Energy Agency noted this deep uncertainty in its official assessment. The agency warned that the global outlook remains highly precarious.

Alternative Export Routes

Suppliers aggressively explore alternative routes to bypass the blocked chokepoints. They utilize the west coast of Saudi Arabia for immediate exports. Producers also push volume through Fujairah on the United Arab Emirates coast. The Iraq to Türkiye pipeline network provides another crucial escape valve. Exporters increased shipments through these alternative channels to 7.2 mb/d. Before the war, these same routes handled less than 4 mb/d.

However, these workarounds cannot replace the massive volume lost in the Gulf. The total loss in oil exports exceeds 13 mb/d. Companies implemented associated production curtailments across the region. Physical damage to energy infrastructure compounds the export difficulties. Logistical experts work relentlessly to establish new supply chains.

Cumulative Supply Losses

The industry measures the destruction in staggering statistical terms. Cumulative supply losses surpassed 360 mb in March alone. Experts project additional losses of 440 mb for April. Rebuilding the damaged infrastructure will require massive capital investment. It will also take years of dedicated engineering work. The International Energy Agency modeled multiple recovery scenarios. Their baseline scenario assumes regular deliveries might resume by mid-year.

However, even the optimistic models do not predict a return to pre-conflict levels. The agency explicitly acknowledged the limitations of their optimistic projections. They presented an alternative case for prolonged disruptions. In this dark scenario, risks to energy production and trade remain high.

Bracing for Prolonged Turmoil

A prolonged conflict presents catastrophic risks for the global economy. Developing nations face the greatest threat from sustained energy inflation. Factories cannot operate without reliable and affordable fuel supplies. Agricultural sectors face surging costs for fertilizers and transportation. Governments scramble to implement emergency measures and secure supply lines. Many politicians consider drastic rationing protocols to preserve national security. The International Energy Agency delivered a stark message to global leaders.

The report warned, “In this case, energy markets and economies around the world need to brace for significant disruptions in the months to come.” The XXI century has never witnessed an energy crisis of this magnitude. Recovery requires unprecedented international cooperation and massive logistical restructuring. The market remains in an extreme state of backwardation. Buyers will pay anything to secure physical barrels today.

Economic Ramifications

High energy costs systematically erode consumer purchasing power. Retail spending plummets as families allocate more money for basic transportation. Major central banks monitor the situation with extreme concern. Structural energy inflation forces policymakers to maintain high interest rates. The International Monetary Fund already downgraded its world growth forecast. The oil shock directly caused this massive macroeconomic downgrade.

Global supply chains experience severe delays and massive cost increases. Shipping companies impose emergency surcharges on almost all international freight. Airlines slash flight schedules to preserve their limited jet fuel inventories. Every economic sector feels the crushing weight of the oil crisis. Small businesses lack the capital reserves to survive prolonged price spikes. Unemployment figures rise as transportation costs bankrupt local enterprises.

Accelerating Energy Transitions

The current crisis forces nations to reevaluate their long-term energy security. Dependence on unstable regions proves fatal to economic stability. Governments now drastically accelerate their investments in alternative energy infrastructure. Solar and wind projects receive unprecedented emergency funding. Nuclear power experiences a sudden resurgence in political popularity. The crisis highlights the severe vulnerabilities of fossil fuel supply chains. Automakers report a massive surge in demand for electric vehicles.

Consumers desperately want to escape the volatility of gasoline prices. However, battery supply chains also face indirect pressures from the global shipping crisis. The transition requires time that the global economy does not currently have. Short-term survival still depends entirely on securing adequate oil supplies. The events of 2026 fundamentally shattered the illusion of market stability.

The Path Forward

Market analysts watch geopolitical developments with intense scrutiny. Resolving the immediate conflict remains the absolute highest priority. Diplomatic channels operate around the clock to broker a sustainable peace. The International Energy Agency clearly identified the most critical factor. The agency stated that resuming flows through the Strait of Hormuz remains essential. This specific action serves as the single most important variable.

It holds the key to easing pressure on global energy supplies. It will directly lower prices and stabilize the broader global economy. Until ships sail freely, the world remains trapped in an energy stranglehold. The data points toward a long and difficult recovery process. 2026 will undoubtedly enter history books as a year of unprecedented disruption. Global energy strategies will change permanently in the aftermath of this shock.

More news: Twin Topside Decommissioning Projects Set New Efficiency Standards in the North Sea

More: IEA